TOM keyword: Flexibility in power markets

Flexibility support schemes: exploring the concept and early experience across Europe

This is the fourth and conclusive installment of the Topic of the Month: exploring flexibility in Europe’s power system

The integration of intermittent renewable energy sources into the electricity system creates new system and network flexibility needs, which we explored in the first instalment. Additionally, as we are transitioning to a carbon-neutral electricity system, flexibility and other system services should eventually be provided by non-fossil resources, namely energy storage and demand response.

What if private markets and contracts alone do not provide sufficient incentives for the necessary (and fast) deployment of non-fossil flexible resources? Member States may have to introduce State Aid measures, i.e. support schemes, to trigger the adequate investments. In this instalment, we explore the need and the concept of non-fossil flexibility support schemes and compare some of the early EU experiences.

Are capacity markets enough to support non-fossil flexibility?

First, non-fossil flexible resources can be supported through capacity mechanisms (CRMs). CRMs grant long term contracts (ranging from 1 to 15 years for new-built) to qualified resources for their availability during scarcity events, measured in MWs. The most common form of CRM, capacity markets, must be open to storage and demand-response.[1] Such capacity markets are currently present in 5 Member States (MS), and their perimeter is expected to expand in the coming years.

CRMs can be an important driver for non-fossil flexible resources deployment, as they offer long-term, predictable income on top of other market revenues. Capacity markets have moreover been adapted to foster the integration of non-fossil resources through, for example, exemptions or tailored processes.[2]

In practice, it is also interesting to observe that non-fossil resources have performed increasingly well in recent capacity market auctions. Battery storage, in particular, has overtaken gas-fired plants in the “new-built” category in recent capacity market auctions. It represents, for example, around 60% (357MW) of the new capacity selected in Belgium for 2027/28 (T-4 auction). However, when considering the total capacity procured by capacity mechanisms, including both existing and new-built, the relative share of demand response and storage remains low, representing only around 4% (see ACER).

Capacity markets target and remunerate only one service: availability during scarcity events. They might therefore not be best suited to incentivize investments in assets providing other flexibility services which are different in nature. Moreover, they have mainly supported fossil-fuelled assets. Hence, support schemes targeting more specifically flexibility services, and non-fossil assets, might be needed to ensure their adequate deployment.

What are non-fossil flexibility support schemes (NFFSS)?

The Electricity Market Design Reform, adopted in 2024, introduced in the Electricity Regulation new articles[3] which allow MS to operate Non Fossil Flexibility Support Schemes (NFFSS). MS must conduct a flexibility needs assessment following a European methodology. Based on their assessment, MS should define indicative national objective for non-fossil flexibility, including the respective specific contribution of both demand response and energy storage.

Where the observed investments are insufficient to achieve these objectives, MS can apply NFFSS consisting of payments for the available non-fossil flexible capacity. The Regulation also includes specific requirements for NFFSS design. They should, for example, be limited to new investments, consider locational criteria, and preserve exposure to price variation and market risk. Published in 2025, the new State Aid Framework (CISAF)[4], provides additional guidance for the design and operation of NFFSS.

Have Member States provided targeted support to non-fossil flexibility before?

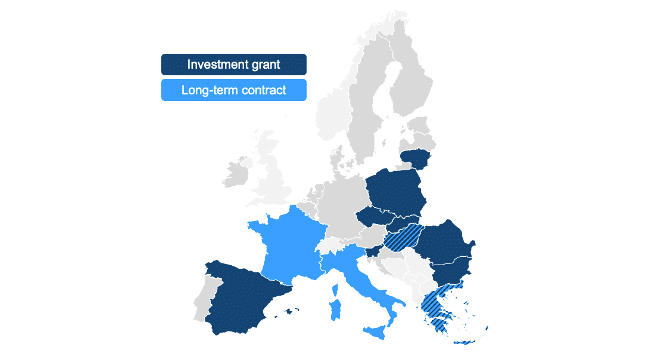

To target specifically battery storage, pumped hydro storage, and demand-response, more than 10 MS have organised dedicated support auctions before the formal introduction of NFFSS in the Electricity Regulation. This includes MS which already had a capacity market perceived as insufficient to meet other flexibility needs, such as France, Italy, and Poland. These support schemes predate the new concept of « NFFSS » and do not meet the applicable requirements of the Electricity Regulation described before. Nevertheless, they are an interesting first experience to look into.

Public support measures[5] must be notified to, and approved by, the European Commission. To be considered compatible with the EU internal market, the measures should be aligned with applicable State Aid Guidelines or Frameworks. Table 1 shows which State Aid communication MS have relied on for supporting non-fossil flexibility. A novelty in 2022 was the Temporary Crisis and Transition Framework (TCTF), which featured a section explicitly dedicated to storage (and renewable) support. The latter was used by 8 MS. Before the TCTF, or to introduce schemes that did not match the TCTF requirements, 6 MS have used directly the general Aid Guidelines applicable in Energy (CEEAG as of 2022).

Table 1 – Overview of State Aid measures targeting specifically storage and/or demand-response

| Compatibility with State Aid Guidelines/Frameworks | State Aid case | |

|---|---|---|

| EEAG (2014–2021) |

Section 3.9. Aid for generation adequacy | FR |

| Section 3.8. Aid to energy infrastructure | LT | |

| CEEAG (2022–today) |

Section 4.8 Aid for the security of electricity supply | FR |

| Section 4.9. Aid for energy infrastructure | EL, RO, ES, IT, FR | |

| TCTF (2022–2025) |

Section 2.5. Aid for accelerating the rollout of renewable energy and energy storage relevant for REPowerEU | HU, SK, SL, PL, BG, LT, ES, CZ |

| CISAF (2025–today) |

Section 4.1. Aid to accelerate the roll-out of renewable energy | RO |

| Section 4.3. Aid for non-fossil flexibility support schemes | n.a. | |

How do these early experiences with supporting non-fossil flexibility compare?

When comparing the design of these earlier schemes, three differences can be identified: the targeted flexibility need, the targeted flexibility resource and the type of support granted. We now give an illustration of these differences.

First, these schemes differed in terms of which need was targeted. Most auctions explicitly aimed to procure resources providing daily flexibility, a large number additionally required contribution to balancing services, and in some cases ancillary services. Congestion management was also considered, for example, in Greece, where the auction had a locational component.

Second, the type of resources targeted differed. In most of these auctions, battery storage was the only allowed technology, often with a focus on large-scale or transmission-connected batteries. According to ACER, the battery storage capacity procured by flexibility measures reaches a total of 8GW (over 2024-2030). Spain, Italy, Slovakia and France have also opened the auctions to other technology such as hydro-pumped or thermal storage, and demand-response.

Third, these support schemes differed in the type of support granted. Eight MS offered only investment grants. Two MS (Greece and Hungary) offered both investment grants and 10-years Contracts-for-Difference (CfDs) based on “benchmark” reference battery market revenues. Finally, two MS (Italy and France) offered only long-term contracts. The Italian storage auction MACSE offers a fixed 15 years monthly premium in exchange for availability on the “time-shifting” platform.[6] France offered a bonus on top of the capacity market revenues, a form of CfD, granted for 5 years.

What’s next?

First, at the time of writing, no NFFSS has been approved under the new State Aid Framework (CISAF Section 4.3). The first cases approved as compatible by the European Commission will be instrumental in setting precedence, as they might provide inspiration for other MS when introducing similar measures. The next question to address in this research is which type of product, and long-term contract, is best suited for incentivizing non-fossil flexible resources deployment while limiting undue distortions in both operational and investment decisions.

Second, NFFSS might overlap with other schemes already present in many MS. This is the case of capacity markets, which already incentivize battery storage deployment; and renewable support schemes when they include provisions related to co-located storage. Coordination between support schemes is another crucial question to address, to avoid excessive or inadequate procurement.

This research was performed in the context of the EVOLVE project, supported by the Norwegian Research Council of Norway Grant number 353023.

[1] The Electricity Regulation Article 22, para. 1(h) states that capacity mechanisms shall « be open to participation of all resources that are capable of providing the required technical performance, including energy storage and demand side management »

[2] For example, in Belgium, demand-response and storage are exempted from the Reliability Option payback obligation. In Poland, demand-response has a lighter qualification process than supply-side resources. In the previous French capacity market, non-fossil resources were eligible to long-term contracts granting a premium on top of the capacity market price, while in the new scheme, a minimum volume of non-fossil flexible resources will be selected in priority in the Y-1 auction.

[3] See Electricity Regulation article 19

[4] See section 4.3 « Aid for non-fossil flexibility support schemes »

[5] It should be noted that we focus in this piece on State Aid measures. Support schemes are notified and approved under State Aid when there is a direct intervention by the State (e.g. public funds, or national legislation). When measures to procure non-fossil flexibility are introduced directly by a system operator, they do not necessarily constitute State Aid. This is the case, for example, of ESB networks (Irish DSO) « Demand flexibility product ». It grants 15-years « floor and share » contracts to demand response and battery storage operators for their availability to mitigate congestions on the distribution grid.

[6] For more information, see for example APE, 2024, « The electricity storage capacity procurement mechanism (MACSE) ». .

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights

More on the topic

How well are consumers protected in demand response services?

This is the third installment of the Topic of the Month: Exploring flexibility in Europe’s power system.

The Citizen Energy Package emphasises the need to actively promote demand-side flexibility across the EU.[1] By enabling citizens to confidently benefit from flexible retail contracts and smart energy devices that optimise energy use, the European Commission expects potential savings of up to 40% for consumers. In this context, the third instalment of the Topic of the Month is about demand response (DR) services from a consumer law perspective.

The FSR Study on the relevance of consumer rights and protections in the context of innovative energy-related services, published alongside the Citizen Energy Package, assesses the extent to which the current EU provisions on consumer rights and protection, both in sector-specific legislation and in horizontal consumer law, are sufficient to protect consumers in the context of innovative energy-related services.

The innovative energy-related services assessed under the FSR Study include demand response services.[2] On the basis of the Study results, in this instalment of the Topic of the Month, we first describe implicit and explicit demand response services under the electricity Market Directive, then, we present the stages of the Energy Consumer Journey (ECJ), finally, we critically assess the level of protection of consumers in demand response services, according to the ECJ. We conclude by mentioning some relevant forthcoming initiatives announced by the European Commission.

How does the Electricity Market Directive regulate demand response services?

Under the Electricity Market Directive (EMD), DR services can be delivered through different types of contracts: (i) energy supply contracts offering DR services through dynamic electricity prices (implicit DR, Article 11 of the EMD), and (ii) DR services provided by independent aggregators (explicit DR, Articles 13 and 17 of the EMD).

From a contractual standpoint, these services differ significantly.

Implicit DR provided through dynamic price contracts is, per se, embedded in dynamic-price energy supply and in the relevant agreement. Therefore, all consumer rights and protections granted to customers involved in energy supply apply to those consumers.

By contrast, DR services provided by independent aggregators are based on separate contractual relationships between consumers and aggregators, which operate independently of energy suppliers. Consequently, their obligations differ from those of suppliers offering dynamic pricing. In addition to EMD provisions, these contracts are subject to the full scope of EU horizontal consumer protection law.

What is the Energy Consumer Journey (ECJ)?

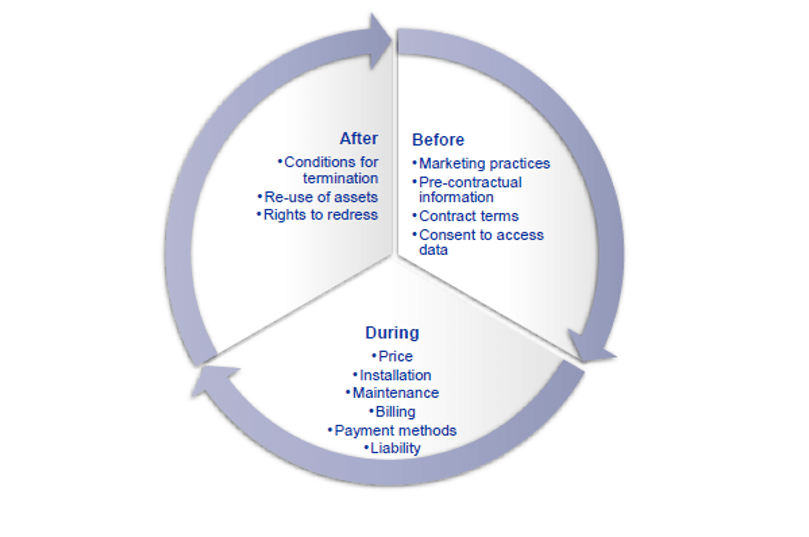

In general, a “consumer journey” refers to the process a consumer undergoes when interacting with a brand, product, or service. In the FSR Study, we have developed a consumer journey tailored to the energy sector.[3] It encompasses all touchpoints and channels a consumer goes through when interacting with an innovative energy-related service provider, divided into three stages: (i) before entering into the agreement; (ii) during the performance of the service; (iii) after the termination of the agreement (see figure 1).

Figure I – Energy Consumer Journey (de Almeida, Porcari, Pototschnig, Rossetto, 2026, p. 26)

The FSR Study has followed the structure of the ECJ to conduct an assessment of how EU horizontal and sector-specific legislation relevant to consumer rights and protections applies to each innovative energy-related service, as well as of possible gaps in the current regulatory framework concerning consumer rights and protection.

Are there any gaps in consumer protection?

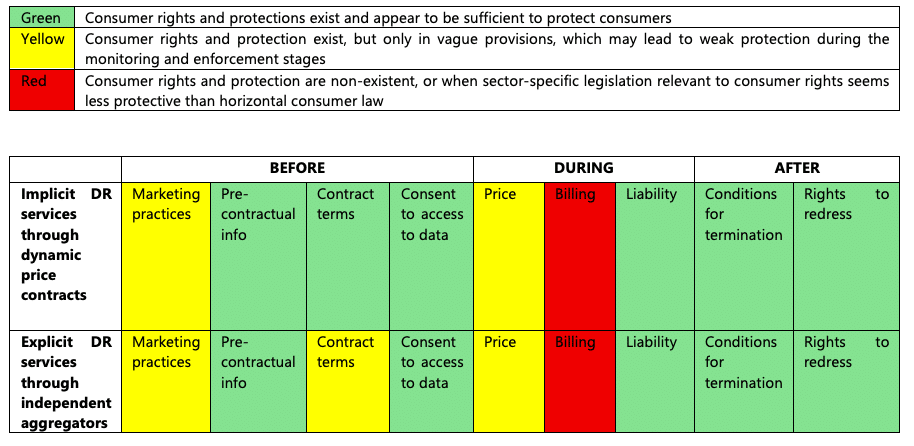

To better visualise the assessment of common consumer law issues arising from innovative energy-related services, we have developed a comparison table summarising the results of the legal analysis for each innovative energy-related service and each stage of the ECJ.[4]

We have adopted a colour-coding system to indicate the current level of consumer protection in relation to the different innovative energy-related services included in the analysis. The results related to demand response services are represented by the table below, and the most critical aspects (yellow and red) are described in more detail after.

Marketing practices

The costs and benefits of consumers engaging in dynamic price contracts and aggregation contracts are not readily understandable to reasonable consumers unfamiliar with how the energy market functions. These contracts could envision prices indexed to wholesale prices from specific spot markets, but prices could vary depending on how suppliers or aggregators design their products. This might raise concerns that the advertising of these products could deceive consumers into switching from fixed-price to dynamic-price contracts, due to a lack of transparent information about the nature and risks of supply contracts with dynamic prices and aggregation contracts.

Contract terms

For implicit DR services under dynamic price contracts, the existing sectoral and horizontal legal framework appears sufficient to protect consumers. First and foremost, the EMD requires that terms and conditions be fair and well known in advance (Article 10(3)). Moreover, the same provisions establish a list of terms that must be included in the contract. Regarding the EU’s horizontal consumer rights, in addition to the Consumer Rights Directive, the Unfair Contract Terms Directive is also applicable, including the rule that terms must always be drafted in plain and intelligible language (Article 5 of the UCTD). On the other hand, for explicit DR services, the EMD does not include specific provisions on contract terms equivalent to those of implicit DR service providers; therefore, only horizontal consumer law applies.

Price

Implicit DR service providers – like energy suppliers – shall ensure that final customers have access to transparent information on applicable prices and tariffs (Article 10(5) of the EMD). On the contrary, the EMD does not regulate how aggregators must charge consumers. The subject falls into horizontal consumer law. As a consumer relationship, Article 6(1)(e) of the Consumer Rights Directive applies. Consumers must be informed about the price in a “clear and comprehensible manner” and “where the nature of the goods or services is such that the price cannot reasonably be calculated in advance, the manner in which the price is to be calculated”.

Billing

For both types of DR services, consumer protection rules under Article 18 of the EMD on billing apply. Consumers must receive key billing information, including the total price and, where possible, a breakdown of charges. Billing must be accurate, clear, concise, user-friendly, and presented in a way that facilitates comparison. However, the EMD provides limited guidance on how dynamic pricing or aggregation-related charges should be communicated in practice.

Looking forward

Overall, the FSR Study shows that there is room to improve the level of protection for consumers who entered DR service contracts. Some of the measures announced under the Citizen Energy Package are specifically intended to unlock the full potential of flexibility and demand response at the residential level.

Notably, under Action 6, titled “Promoting flexibility through retail contracts”, the Commission intends to provide guidance to promote the remuneration of flexibility in retail contracts (expected Q1 2026); improve access to the data required for flexibility with an Implementing Regulation on interoperability requirements and procedures (expected 2027); and promote the potential of flexibility and efficiency in relevant projects under the new Partnerships for Better Homes (expected 2026).

FSR researchers will closely monitor these forthcoming initiatives.

[1] The Package is structured around four pillars and nine actions: (Pillar I) lowering energy bills for households (actions 1 to 4); (Pillar II) protecting and empowering consumers (actions 5 to 7); (Pillar III) tackling energy poverty and vulnerability (actions 8 and 9); (Pillar IV) implementing the existing EU laws. For a description of the nine actions, see https://fsr.eui.eu/nine-actions-for-a-citizen-centric-energy-transition/.

[2] The Study distinguishes between the following three categories of innovative energy-related services: broadly available services, emerging services, and services of the future. Demand response services are included in the second category.

[3] See de Almeida, Porcari, Pototschnig, Rossetto (2026), Study on the relevance of consumer rights and protections in the context of innovative energy-related services, p. 25-27, available at https://energy.ec.europa.eu/publications/study-relevance-consumer-rights-and-protections-context-innovative-energy-related-services_en.

[4] This Comparison Table is included in Annex II of the Study, available at https://op.europa.eu/en/publication-detail/-/publication/7b401b96-1c31-11f1-8c3a-01aa75ed71a1/language-en.

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights

More on the topic

Flexibility and grids: understanding available grid capacity, connection queues and what can be done

This is the second installment of the Topic of the Month: exploring flexibility in Europe’s power system

The development of electricity grids and the flexibility needs of an electricity system are deeply interlinked. When grids expand too slowly and become congested, network flexibility needs tend to increase. Grid constraints can also affect system flexibility needs when they lead to the curtailment of intermittent renewable generation or limit the participation of flexibility providers through prequalification.[1] A lack of transparency in available grid capacity might further complicate this interaction. Finally, grids can delay the achievement of flexibility targets when new flexibility service providers are waiting in grid connection queues.

In this instalment, we look at the interaction between grids and flexibility from three angles. First, we describe how information on available grid capacity is currently shared with end‑users. Second, we discuss why bottlenecks may arise not only from physical capacity limitations but also from grid connection processes themselves. Finally, we provide a high-level overview of the approaches that can be considered to address grid capacity constraints and grid connection queues.

Transparency on available grid capacity

A recent study by Fraunhofer for the European Commission states that, although grid congestion is starting to emerge as a challenge for system operators, most Member States have not yet experienced systemic congestion issues at the national scale.[2] At the same time, transparency on network constraints and grid availability is increasing across Europe. This trend is linked to the provisions of the Electricity Market Design reform, which require distribution and transmission system operators to ‘publish in a transparent manner clear information on the capacity available for new connections in their area(s) of operation’. [3]

To fulfil these requirements, system operators are increasingly developing hosting capacity maps to indicate areas with available grid capacity in their networks. These maps show not only where new (flexible) users may be able to connect without delay, but also where congestion is already present and flexibility could be particularly valuable. In practice, however, the design and features of these hosting capacity maps are currently very diverse. Differences can be observed, for example, in colour codes, granularity, user groups, interaction between system operators, and the consideration of congestion management tools or future grid investments.[4] In addition, system operators may apply different approaches when calculating available grid capacity. In a recent FSR working paper, we identified seven factors where different assumptions might be applied, and we qualitatively assessed the potential impact of overlooking these factors on the calculation of available grid capacity (i.e. whether there is a tendency to over- or underestimate it). Finally, it is worth noting that, as part of the Grid Action Plan, the EU DSO Entity and ENTSO-E are developing a portal on grid hosting capacities, where links to all hosting capacity websites, supporting definitions and good practices will be shared.[5]

Bottlenecks arising from grid connection processes

Beyond grid capacity, grid connection processes are increasingly becoming a bottleneck for new flexibility providers to start delivering their services. It is important to note that these queues do not necessarily depend on the physical availability of network capacity. When no grid capacity is available, new requests naturally enter a queue. However, queues can also arise in areas where remaining capacity exists when the number of connection requests grows faster than system operators can process them.

The aforementioned study by Fraunhofer for the European Commission reports that at least 15 Member States already face problems with grid connection queues at distribution level. Similar observations appear in a report by BCG, which compares the size of connection queues for demand, generation and storage projects at transmission level across different regions of the world. Three notable cases discussed in this report are Italy, the United Kingdom and Finland, which have queue sizes that are approximately 12, 15 and 30 times larger than their respective national peak loads in 2024. Beyond illustrating that queue problems can be significant, these figures also point to another issue associated with grid connection procedures: the presence of speculative or immature applications, also called “zombie”, “ghost” or “paper” projects. This challenge was also acknowledged in the European Commission’s Guidance on efficient and timely grid connections, which was published as part of the European Grids Package.

Approaches to address grid capacity constraints and grid connection bottlenecks

Several approaches can be considered to address the bottlenecks described above. Broadly, these measures fall into two categories: ensuring sufficient grid capacity and establishing efficient grid connection procedures. The former can reduce both grid congestion and the length of connection queues, while the latter primarily targets the processing of applications within the queue.[6]

Ensuring sufficient grid capacity involves both making better use of existing infrastructure and enabling efficient and timely buildout of new infrastructure. Existing grid capacity can be used more efficiently through grid tariff incentives, flexible connection agreements, congestion management (i.e., local flexibility markets) and releasing reserved but unused grid capacity. In parallel, the efficient and timely buildout of new infrastructure can be enabled through a combination of reduced deployment times, more coordinated and forward-looking network planning and anticipatory investments. It must be noted that uncertainty around how the perceived risks of anticipatory investments should be mitigated and shared seems to remain a barrier to their widespread deployment. The Commission’s Guidance on anticipatory investments can be seen as a first step towards creating more favourable conditions at Member State level.

Establishing efficient grid connection procedures involves both managing the size of the queue and revisiting the queue evaluation process. Measures to manage the queue size include introducing fees, milestones or maturity criteria to reduce speculative behaviour, removing invalid applications from the queue, and ensuring capacity requests reflect realistic project needs. In addition, the process of evaluating applications can be accelerated through deadlines, standardisation, digitalisation and targeted exceptions. Finally, the order in which connection requests are processed is also increasingly under discussion. The Commission’s Guidance on efficient and timely grid connections, for example, provides an overview of alternatives to the first‑come‑first‑served principle that Member States can consider.

[1] A more detailed description of network and system flexibility needs can be found in the first instalment of this Topic of the Month: https://fsr.eui.eu/flexibility-in-power-systems-whats-there-beyond-the-buzzword/.

[2] More specifically, the study gathers data and compares practices from all 27 EU Member States through desk research and interviews, focusing on distribution grids and covering: 1) network planning, 2) network tariff design and regulatory incentives, and 3) treatment of grid connection requests.

[3] See Regulation (EU) 2024/1747 Article 50 on the requirements for transmission system operators and Directive (EU) 2024/1711 Article 31 on the requirements for distribution system operators.

[4] For a more detailed comparison of grid hosting capacity maps across Europe, see for example Eurelectric (2023), “Power System of the Future: Keys to delivering capacity on the distribution grid”, available at https://www.eurelectric.org/wp-content/uploads/2024/06/report-block-1_part-1-grid-capacity_final-draft_3082023.pdf; Ember & RAP (2024), “Transparent Grids for All. Grid(un)lock: Hosting Capacity Maps”, available at https://ember-energy.org/latest-insights/transparent-grids-for-all/; and European Commission & Fraunhofer (2025), “Study on network development planning, tariff structures and connection requests for electricity distribution grids”, available at https://data.europa.eu/doi/10.2833/9351025.

[5] For more information, see https://www.entsoe.eu/grid-action-plan-on-hosting-capacities/.

[6] However, grid connection queue management tools could in some cases also address grid congestion, for example, if flexible resources that can mitigate grid congestion get priority treatment in the queue.

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights

More on the topic

Flexibility in power systems: what’s there beyond the buzzword?

This is the first installment of the Topic of the Month: exploring flexibility in Europe’s power system

The increasing penetration of intermittent renewable energy sources, together with the electrification of end uses like heating and transport, is reshaping Europe’s electricity system. As these trends accelerate, flexibility is now widely recognised as a key enabler for integrating renewable energy, ensuring system reliability and managing grid congestion.

In this Topic of the Month, we explore the role of flexibility in Europe’s power system from several perspectives.

This first instalment focuses on three fundamental questions that set the scene for the coming month: What do we mean by “flexibility” in power systems? How much flexibility will be needed in the coming decades? Where can this flexibility come from, and how can we mobilise it?

What do we mean by ‘flexibility’ in power systems?

Over the past few years, the term “flexibility” has entered multiple areas of European energy policy and regulation. It appears, for example, in Directive (EU) 2019/944, which promotes the use of flexibility in distribution networks. It was also the topic of the assessment undertaken by the European Environment Agency (EEA) and ACER, which aimed to quantify daily, weekly and monthly flexibility needs.

However, as the term became more common, its meaning also became increasingly ambiguous. An important contribution of the Electricity Market Design reform in this regard was the introduction of a definition for flexibility[1], which was then further refined by the flexibility needs assessment methodology. More specifically, the methodology distinguishes between two types of flexibility needs: network and system needs. Network flexibility needs are defined as the ability to adjust to grid availability, particularly to prevent or resolve congestion or voltage issues, across all applicable timeframes. System flexibility needs are defined as the ability of the electricity system to adjust to the variability of generation and consumption patterns across relevant market timeframes. Within system flexibility needs, three subcategories are outlined:[2]

- RES integration needs, or the amount of flexibility required for a Member State to meet its renewable energy integration target, which can be on a daily, monthly or annual basis.

- Ramping needs, associated with variations in residual load under perfect forecast conditions.

- Short‑term flexibility needs, linked to unexpected variations in residual load, such as forced outages during the intraday and balancing timeframe.

How much flexibility will be needed in the coming decades?

In Europe, a systematic assessment of flexibility needs represents a recent novelty. The national flexibility needs assessments due by July 2026, followed by the EU‑wide analysis performed by ACER due to July 2027, are expected to provide a clearer picture.

In the meantime, several studies offer preliminary insights.[3] While methodologies between these studies vary, a consistent conclusion emerges: system flexibility needs in Europe are expected to double by 2030 and increase six‑fold by 2050 compared to early‑2020s levels. The main driver of this rapid increase in 2030 is the changing generation mix, especially the massive deployment of solar PV and its distinct daily production profile. In the longer term, towards 2040 and 2050, growing electricity demand is expected to become the dominant driver. [4]

The increase in anticipated system flexibility needs might be amplified by the slow expansion of electricity grids. An analysis carried out by the Joint Research Centre (JRC) shows that if transmission infrastructure continues to expand at its current pace, congestion and redispatch needs will rise significantly. Even in a favourable scenario where transmission grids grow by roughly a third by the end of the current decade, redispatch costs are expected to rise from about 5 to 9 billion euros per year. Renewable generation curtailment is also expected to increase sharply, by 50 to 121 TWh in 2030, due to network bottlenecks.[5] These numbers highlight how grid development and flexibility provision are deeply interlinked. We will therefore discuss the role of grids in more detail in the second instalment of the Topic of the Month.

Where can this flexibility come from, and how can we mobilise it?

Flexibility can be delivered by a broad range of sources and is ideally non‑fossil, in line with the EU’s decarbonisation objectives. Key flexibility providers include dispatchable low‑carbon generation, which can adjust output quickly and has relatively low start‑up and shut‑down costs. Large‑scale storage technologies, such as pumped‑storage hydropower and utility‑scale batteries, are also expected to contribute significantly. Demand‑side response may represent another important source, drawing on the potential of residential, industrial, commercial and public service consumers, although further progress is still needed to unlock this potential in practice.[6] We will examine the importance of consumer protection when providing flexibility in more detail in the third instalment of this series.

In general, flexibility can be mobilised in two ways: implicitly, when final customers or assets respond to varying electricity prices or network charges that reflect the value of electricity or network conditions at different moments; or explicitly, when flexibility providers adjust their consumption or generation through participation in electricity markets or following activation by system operators. Explicit flexibility can be enabled either through short-term energy activations or through long-term availability payments. In the fourth instalment of this Topic of the Month, we will look in more detail at one of these long‑term availability payments, namely non‑fossil flexibility support schemes.

When talking about flexibility, lots of interesting discussions lie ahead, but first we wish you a lovely spring break!

[1] More specifically, Regulation (EU) 2024/1747 defines flexibility as “the ability of an electricity system to adjust to the variability of generation and consumption patterns and to grid availability, across relevant market timeframes”.

[2] These three subcategories will be part of the flexibility needs assessments introduced in the Electricity Market Design reform. In addition, adequacy needs (already covered in the European and National Resource Adequacy Assessments) and certain TSO-specific reliability needs (such as inertia or system restoration) can also be considered as system flexibility needs.

[3] Among the many relevant contributions, the reader can consider: JRC, ‘Flexibility requirements and the role of storage in future European power systems’ (Publications Office of the European Union, 2023); EEA and ACER, ‘Flexibility solutions to support a decarbonised and secure EU electricity system’ (Publications Office of the European Union, 2023); JRC, ‘Redispatch and congestion management, Future proofing the European power market’ (Publications Office of the European Union, 2024); and ENTO-E, ‘System flexibility needs for the energy transition’ (ENTSO-E, 2024).

[4] JRC, ‘Flexibility requirements and the role of storage in future European power systems’ (Publications Office of the European Union, 2023), p. 11-13.

[5] JRC, ‘Redispatch and congestion management, Future proofing the European power market’ (Publications Office of the European Union, 2024). It is to be noted that the study by the JRC only considers the transmission network and cannot fully capture congestion emerging at the distribution level.

[6] Finally, it must be noted that cross-border interconnectors will also play an important role in the provision of flexibility.

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights

More on the topic