Flexibility support schemes: exploring the concept and early experience across Europe

This is the fourth and conclusive installment of the Topic of the Month: exploring flexibility in Europe’s power system

The integration of intermittent renewable energy sources into the electricity system creates new system and network flexibility needs, which we explored in the first instalment. Additionally, as we are transitioning to a carbon-neutral electricity system, flexibility and other system services should eventually be provided by non-fossil resources, namely energy storage and demand response.

What if private markets and contracts alone do not provide sufficient incentives for the necessary (and fast) deployment of non-fossil flexible resources? Member States may have to introduce State Aid measures, i.e. support schemes, to trigger the adequate investments. In this instalment, we explore the need and the concept of non-fossil flexibility support schemes and compare some of the early EU experiences.

Are capacity markets enough to support non-fossil flexibility?

First, non-fossil flexible resources can be supported through capacity mechanisms (CRMs). CRMs grant long term contracts (ranging from 1 to 15 years for new-built) to qualified resources for their availability during scarcity events, measured in MWs. The most common form of CRM, capacity markets, must be open to storage and demand-response.[1] Such capacity markets are currently present in 5 Member States (MS), and their perimeter is expected to expand in the coming years.

CRMs can be an important driver for non-fossil flexible resources deployment, as they offer long-term, predictable income on top of other market revenues. Capacity markets have moreover been adapted to foster the integration of non-fossil resources through, for example, exemptions or tailored processes.[2]

In practice, it is also interesting to observe that non-fossil resources have performed increasingly well in recent capacity market auctions. Battery storage, in particular, has overtaken gas-fired plants in the “new-built” category in recent capacity market auctions. It represents, for example, around 60% (357MW) of the new capacity selected in Belgium for 2027/28 (T-4 auction). However, when considering the total capacity procured by capacity mechanisms, including both existing and new-built, the relative share of demand response and storage remains low, representing only around 4% (see ACER).

Capacity markets target and remunerate only one service: availability during scarcity events. They might therefore not be best suited to incentivize investments in assets providing other flexibility services which are different in nature. Moreover, they have mainly supported fossil-fuelled assets. Hence, support schemes targeting more specifically flexibility services, and non-fossil assets, might be needed to ensure their adequate deployment.

What are non-fossil flexibility support schemes (NFFSS)?

The Electricity Market Design Reform, adopted in 2024, introduced in the Electricity Regulation new articles[3] which allow MS to operate Non Fossil Flexibility Support Schemes (NFFSS). MS must conduct a flexibility needs assessment following a European methodology. Based on their assessment, MS should define indicative national objective for non-fossil flexibility, including the respective specific contribution of both demand response and energy storage.

Where the observed investments are insufficient to achieve these objectives, MS can apply NFFSS consisting of payments for the available non-fossil flexible capacity. The Regulation also includes specific requirements for NFFSS design. They should, for example, be limited to new investments, consider locational criteria, and preserve exposure to price variation and market risk. Published in 2025, the new State Aid Framework (CISAF)[4], provides additional guidance for the design and operation of NFFSS.

Have Member States provided targeted support to non-fossil flexibility before?

To target specifically battery storage, pumped hydro storage, and demand-response, more than 10 MS have organised dedicated support auctions before the formal introduction of NFFSS in the Electricity Regulation. This includes MS which already had a capacity market perceived as insufficient to meet other flexibility needs, such as France, Italy, and Poland. These support schemes predate the new concept of « NFFSS » and do not meet the applicable requirements of the Electricity Regulation described before. Nevertheless, they are an interesting first experience to look into.

Public support measures[5] must be notified to, and approved by, the European Commission. To be considered compatible with the EU internal market, the measures should be aligned with applicable State Aid Guidelines or Frameworks. Table 1 shows which State Aid communication MS have relied on for supporting non-fossil flexibility. A novelty in 2022 was the Temporary Crisis and Transition Framework (TCTF), which featured a section explicitly dedicated to storage (and renewable) support. The latter was used by 8 MS. Before the TCTF, or to introduce schemes that did not match the TCTF requirements, 6 MS have used directly the general Aid Guidelines applicable in Energy (CEEAG as of 2022).

Table 1 – Overview of State Aid measures targeting specifically storage and/or demand-response

| Compatibility with State Aid Guidelines/Frameworks | State Aid case | |

|---|---|---|

| EEAG (2014–2021) |

Section 3.9. Aid for generation adequacy | FR |

| Section 3.8. Aid to energy infrastructure | LT | |

| CEEAG (2022–today) |

Section 4.8 Aid for the security of electricity supply | FR |

| Section 4.9. Aid for energy infrastructure | EL, RO, ES, IT, FR | |

| TCTF (2022–2025) |

Section 2.5. Aid for accelerating the rollout of renewable energy and energy storage relevant for REPowerEU | HU, SK, SL, PL, BG, LT, ES, CZ |

| CISAF (2025–today) |

Section 4.1. Aid to accelerate the roll-out of renewable energy | RO |

| Section 4.3. Aid for non-fossil flexibility support schemes | n.a. | |

How do these early experiences with supporting non-fossil flexibility compare?

When comparing the design of these earlier schemes, three differences can be identified: the targeted flexibility need, the targeted flexibility resource and the type of support granted. We now give an illustration of these differences.

First, these schemes differed in terms of which need was targeted. Most auctions explicitly aimed to procure resources providing daily flexibility, a large number additionally required contribution to balancing services, and in some cases ancillary services. Congestion management was also considered, for example, in Greece, where the auction had a locational component.

Second, the type of resources targeted differed. In most of these auctions, battery storage was the only allowed technology, often with a focus on large-scale or transmission-connected batteries. According to ACER, the battery storage capacity procured by flexibility measures reaches a total of 8GW (over 2024-2030). Spain, Italy, Slovakia and France have also opened the auctions to other technology such as hydro-pumped or thermal storage, and demand-response.

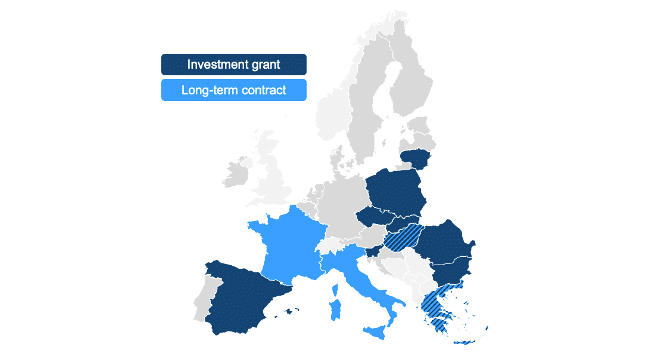

Third, these support schemes differed in the type of support granted. Eight MS offered only investment grants. Two MS (Greece and Hungary) offered both investment grants and 10-years Contracts-for-Difference (CfDs) based on “benchmark” reference battery market revenues. Finally, two MS (Italy and France) offered only long-term contracts. The Italian storage auction MACSE offers a fixed 15 years monthly premium in exchange for availability on the “time-shifting” platform.[6] France offered a bonus on top of the capacity market revenues, a form of CfD, granted for 5 years.

What’s next?

First, at the time of writing, no NFFSS has been approved under the new State Aid Framework (CISAF Section 4.3). The first cases approved as compatible by the European Commission will be instrumental in setting precedence, as they might provide inspiration for other MS when introducing similar measures. The next question to address in this research is which type of product, and long-term contract, is best suited for incentivizing non-fossil flexible resources deployment while limiting undue distortions in both operational and investment decisions.

Second, NFFSS might overlap with other schemes already present in many MS. This is the case of capacity markets, which already incentivize battery storage deployment; and renewable support schemes when they include provisions related to co-located storage. Coordination between support schemes is another crucial question to address, to avoid excessive or inadequate procurement.

This research was performed in the context of the EVOLVE project, supported by the Norwegian Research Council of Norway Grant number 353023.

[1] The Electricity Regulation Article 22, para. 1(h) states that capacity mechanisms shall « be open to participation of all resources that are capable of providing the required technical performance, including energy storage and demand side management »

[2] For example, in Belgium, demand-response and storage are exempted from the Reliability Option payback obligation. In Poland, demand-response has a lighter qualification process than supply-side resources. In the previous French capacity market, non-fossil resources were eligible to long-term contracts granting a premium on top of the capacity market price, while in the new scheme, a minimum volume of non-fossil flexible resources will be selected in priority in the Y-1 auction.

[3] See Electricity Regulation article 19

[4] See section 4.3 « Aid for non-fossil flexibility support schemes »

[5] It should be noted that we focus in this piece on State Aid measures. Support schemes are notified and approved under State Aid when there is a direct intervention by the State (e.g. public funds, or national legislation). When measures to procure non-fossil flexibility are introduced directly by a system operator, they do not necessarily constitute State Aid. This is the case, for example, of ESB networks (Irish DSO) « Demand flexibility product ». It grants 15-years « floor and share » contracts to demand response and battery storage operators for their availability to mitigate congestions on the distribution grid.

[6] For more information, see for example APE, 2024, « The electricity storage capacity procurement mechanism (MACSE) ». .

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights