Report from the 38th Madrid Forum

This is the third installment of the Topic of the Month: A new stage for the EU gas market: which regulation?

On 25th and 26th April, the 38th edition of the European Gas Regulatory Forum (aka Madrid Forum) took place. As always, the Forum is a great opportunity to take stock of the recent regulatory developments impacting the EU energy markets and at the same time get a sense of the direction that the EU energy policy and regulatory thinking might be heading in the upcoming months.

Under the leadership of the European Commission’s DG Energy (DG ENER), the Madrid Forum is open to national regulatory authorities, EU national governments, associations of transmission system operators, gas suppliers and traders, consumers, network users, and gas exchanges and it is hosted once to twice a year by the Spanish energy regulator Comisión Nacional de los Mercados y la Competencia (CNMC).

Among the main topics included in this year’s agenda were: the regulation applying to LNG, an assessment of the status of the EU gas market and of its neighbouring Energy Community countries, the review of REMIT (Regulation for Market Integration and Transparency) and of course the recently adopted Hydrogen and Decarbonised Gas Market Package (HDGMP), including the planned review of some of its Network Codes and guidelines (CAM and CMP to start with).

EU gas market: a post-crisis assessment

Occurring two-and-a-half years after the beginning of the gas crisis, the 38th Madrid Forum surely represented a timely occasion for a first review and assessment of the so-called ‘emergency regulation’ – that is, those regulatory measures published as of Autumn 2021 and aiming to contrast the impact of the gas crisis and of Russian’s aggression to Ukraine on EU gas markets.

Different views were raised on the need to maintain or renew some of the emergency measures – such as the new storage legislation provisions, and particularly its refilling obligations – in a period that can already be considered post-crisis. The Commission rightly agreed with stakeholders that “Emergency measures should not remain in place for longer than needed”.

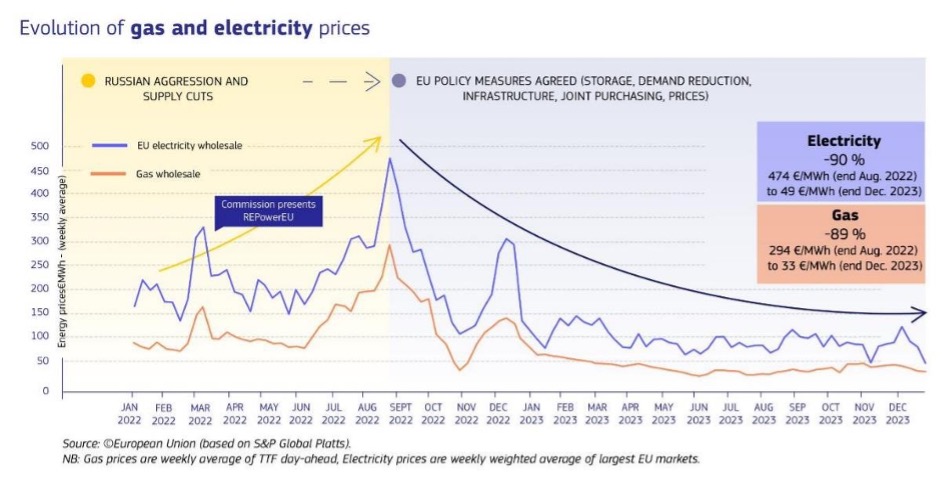

With the most critical moments finally behind us, and now that the main security of supply threats to the EU gas markets can be considered overcome, DG ENER acknowledged the positive cooperation of all parties (Member States, EU Institutions, industry etc) during the crisis, as well as the success of the new rules, which significantly contributed to the REPowerEU target of replacing the 140 bcm of Russian gas pipeline supply, in a very short time. Indeed, in 2022-2023 the overall EU energy demand dropped by 18%, while gas in store has reached the highest levels historically for two consecutive years. At the same time, electricity and gas prices decreased by -90% and -89% respectively in the period Aug 2022/Dec 2023 (see table).

But resilience recovery from the supply shock was not the only target achieved in this period. Looking at decarbonisation and climate objectives, the last two years recorded a number of positive data: an increase of 56 GW in solar energy generation and 17 GW in wind, and a steady significant increase in biogas/biomethane as reported by the European Biogas Association (total EU generation to reach 15bcm by 2030, that is a five-fold increase compared to the pre-crisis levels).

Moreover, several of the recent EU regulatory initiatives keep bringing results. For instance, the new EED recast which makes energy efficiency an integral part of policy and investment decisions and strengthens energy savings obligations in end use; the Energy Performance of Buildings Directive (EPBD recast), aiming at decarbonisation of EU building stock, the increased targets and provisions on Power Purchase Agreements and Guarantees of Origin under the REDIII, or the new EU Methane Regulation, the first one to reduce ME in the energy sector. Extends to crude oil, NG and coal. Aims to improving measurement and reporting, reduce ME via prescriptive abatement measures (already implementable), increasing transparency, incentives cooperation with international partners.

Aggregate-EU, the Electricity Market Design Reform, NZIA were also mentioned with their provisions aimed at improving the overall EU energy markets functioning.

Where are the molecules? The call for a vision encompassing sector coupling/integration

During the Madrid Forum, some criticism was raised with respect to the limited relevance given in the agenda to security of supply. Despite the emergency levels are back under control, and the good news regarding improved resilience, diversification of supply and sources – molecules are still considered as the main insurance against sudden supply shocks, but a clear vision for their role in the future EU energy system is currently missing.

Several parties (from CEDEC to ACER, from Eurelectric to GIE) called for a greater focus and vision on sector coupling and sector integration, as to make sure that all interested actors can work towards the same direction. The ambitious targets for electrification of consumption sectors cannot be achieved without a solid support from molecules, which will become even more fundamental to provide flow stability and reliability, by compensating for the increasing demand and unpredictability coming from RES generation. The general belief of the Forum is that conceiving a vision and a plan for an integrated energy sector – where synergies between electricity and gas are maximised – will allow for more efficiency and a better overview of how to reach sustainability and climate targets.

Decarbonising with renewable and low-carbon gases: (some of) the critical points emerged

As we can read in the Forum conclusions, the Commission invited Member States to a swift transposition and implementation of the Hydrogen and Decarbonised Gas Package, which “will be beneficial for the roll-out of renewable and low-carbon gases”.

The new HDGMP [approved by the EU Parliament and Council few weeks after the Madrid Forum] indeed includes measures aiming at facilitating the integration of renewable and low-carbon gases in Europe, at market and infrastructure level.

In Madrid, only some of the numerous elements stemming from the Package were discussed (but no doubt that more occasions for debate will occur in the next months). For the conciseness imposed by the format of this article, I’ll briefly focus on three main highlights from the discussion:

- Role of NRAs in implementation: regulators will be facing some implementation challenges and the Package does offer some tools to deal with the uncertainties deriving from the novelties that are introduced. For instance, the application of the transitory period measures with exceptions/exemptions, the consultation process on the tariff methodology to apply at interconnection points and – quite critically – the financial transfers of RABs between gas and hydrogen networks etc). Additionally, a higher level of uncertainty will concern the plans for hydrogen infrastructure development, that will need to be based on H2 demand developments – hence to be regularly monitored.

- Infrastructure: Within the EU, the majority of H2 projects are currently serving the so-called hydrogen valleys (industrial clusters). Repurposing of existing infrastructure will trigger some critical regulatory decisions to be taken based on tariff, interoperability and also sustainability considerations- particularly since the projects are at a different stage of maturity. Regarding storage, the EU Commission deems that a sufficient amount of H2 storage projects will be key for a good functioning of the system and that regulators are given the instruments to facilitate H2 storage infrastructure development.

At interconnection level, the latest list of Projects of Common Interest and Projects of Mutual Interest was adopted includes 166 projects in total: 85 electricity projects and, for the first time, 65 H2 and electrolysers projects. 14 CO2 network projects are included, and no blending projects.

On the other hand, the realisation of the so-called H2 corridors will depend on the real evolution of supply and demand for H2 across Europe. Consequently, also to what extent local and long-distance infrastructure will be interconnected is very hard to predict at present. - Gas quality: some of the major industrial consumers brought to the Forum’s attention the potential gas quality issues deriving from the increased introduction of renewable and low-carbon gases into the system, and how important it is for some industries to guarantee a very high degree of compatibility with the gas quality in the existing system. The Forum was reassured that an update of the existing EU Gas Network Codes will take place and particularly the Interoperability (INT), Balancing (BAL), Capacity Allocation Mechanisms (CAM)/Congestion Management Procedures (CMP) will be reviewed, not least for quality issues.

The contribution of FSR to the debate

We had the opportunity to contribute to the Madrid Forum debate with a presentation on the State of the Gas market: after a general overview of the EU gas market and of the main changes originating from the 2021-2022 events, we devoted a special attention to LNG markets and the findings of the almost concluded EU-funded project LNGnet – hinting at the need for Europe to focus on the carbon intensity of the imported LNG volumes and its consequences at commercial and environmental level. FSR is currently contributing to one of the LNGnet working groups looking into how to translate such information into standardised LNG Sales and Purchase Agreements.

In the second part of the presentation, we highlighted the need to reflect on potential future security threats, and we presented a proposal on the decoupling of gas prices (LNG vs pipeline gas), based on two policy briefs (1 and 2)that we published during the gas crisis

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights

More on the topic