Commercialising ocean energy technologies

In this article, Elena Ocenic (IRENA) delves into ocean energy technologies and the process to take them to the commercialisation stage.

How can we bring ocean energy technologies closer to commercialisation? In this article, Elena Ocenic, Associate Programme Officer – Innovation Networks at the International Renewable Energy Agency (IRENA), explains how the process can be facilitated by following 7 key actions.

Oceans’ untapped potential

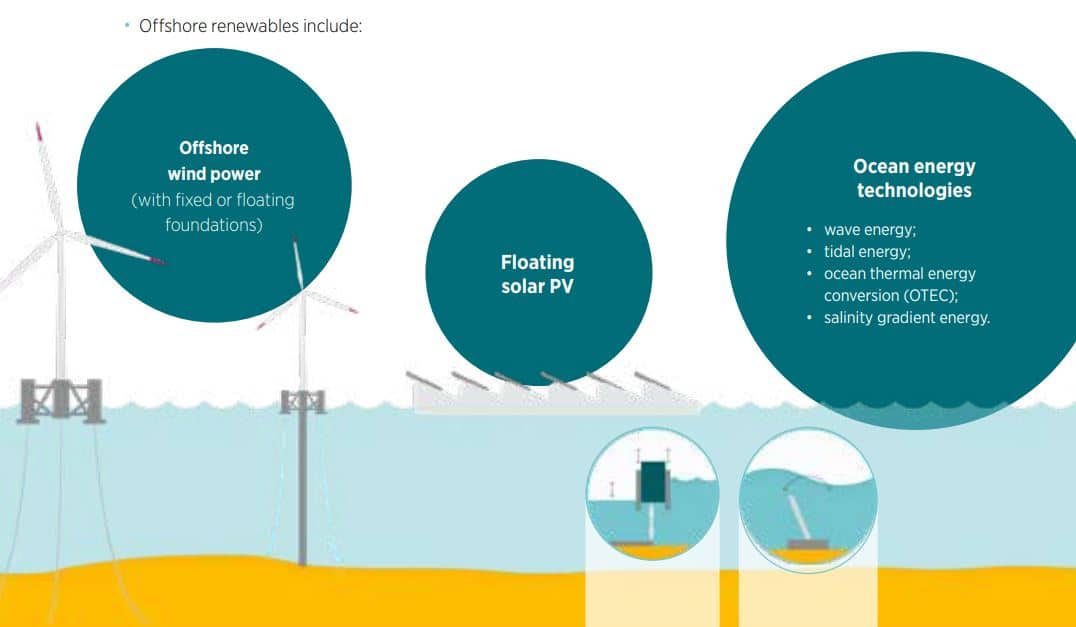

Oceans – usually associated with aquaculture and shipping – hold plentiful, largely untapped renewable energy potential, which could power a dynamic global blue economy both in the European Union and beyond. For instance, offshore renewable energy technologies could help fulfil several international climate and development goals, including the Paris Agreement and the United Nations Sustainable Development Goals 7 and 14 set for 2030. As shown in Figure 1, offshore renewables comprise a) offshore wind on fixed or floating foundations, as well as airborne wind, b) ocean energy like wave, tidal, ocean thermal energy conversion (OTEC), as well as salinity gradient; and c) floating solar photovoltaic technologies.

Figure 1: Classification of offshore renewables

Source: IRENA, 2020a

Among these, ocean energy technologies are still in their nascent stage. However, having recorded a dynamic development in recent years, ocean energy technologies have the potential to play a key role in the decarbonisation of the power sector along with the decarbonization of other end-use applications of the blue economy, such as aquaculture, cooling, shipping tourism and water desalination, among others. Moreover, these innovative power generating technologies could provide significant socio-economic benefits, especially to coastal areas and island territories, including jobs, improved health, strengthened incomes, and the creation of local value chains (IRENA, 2020b, IRENA, 2020c).

Ocean energy technologies: market status and outlook

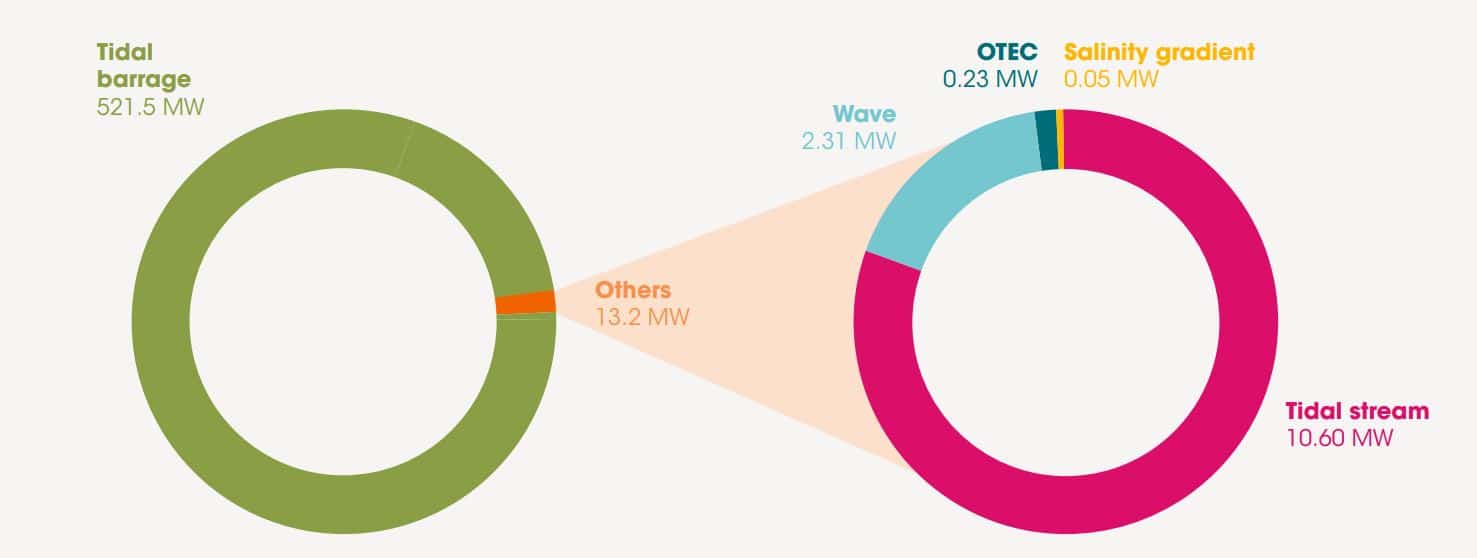

Today, the cumulative global installed capacity of ocean energy is 534.7 megawatts (MW) which is negligible when compared to the cumulative global installed capacity of renewable energy of around 2 600 GW. Currently, the total installed capacity of ocean energy is dominated by tidal barrage (also called “tidal range”) with around 521.5 MW mainly composed of three large projects in Canada, France and the Republic of Korea, while the remaining capacity of around 13.2 MW is shared between tidal stream, wave energy, OTEC and salinity gradient (Figure 2).

Figure 2: Global installed capacity of ocean energy technologies (2020)

Source: IRENA, 2020c

Despite today’s dominance of tidal barrage, there were no major developments in almost 10 years, and the resource potential is relatively low compared to other ocean energy technologies – which is why the attention is shifting towards the other technologies that record a more dynamic project development and high resource potential. More precisely, there are currently multiple projects under development for tidal stream and wave energy technologies which – if realized – will amount to almost 3 GW of installed capacity worldwide in the next 5 years (Figure 3), most of it in Europe (55%), followed by Asia and the Pacific (28%) and the Middle East and Africa (13%), as shown in Figure 4. However, with the right incentives and regulatory frameworks in place, IRENA foresees the potential growth of ocean energy up to 10 GW of installed capacity by 2030 globally.

Figure 3: Active and projected ocean energy capacity beyond 2020

Source: IRENA, 2020c

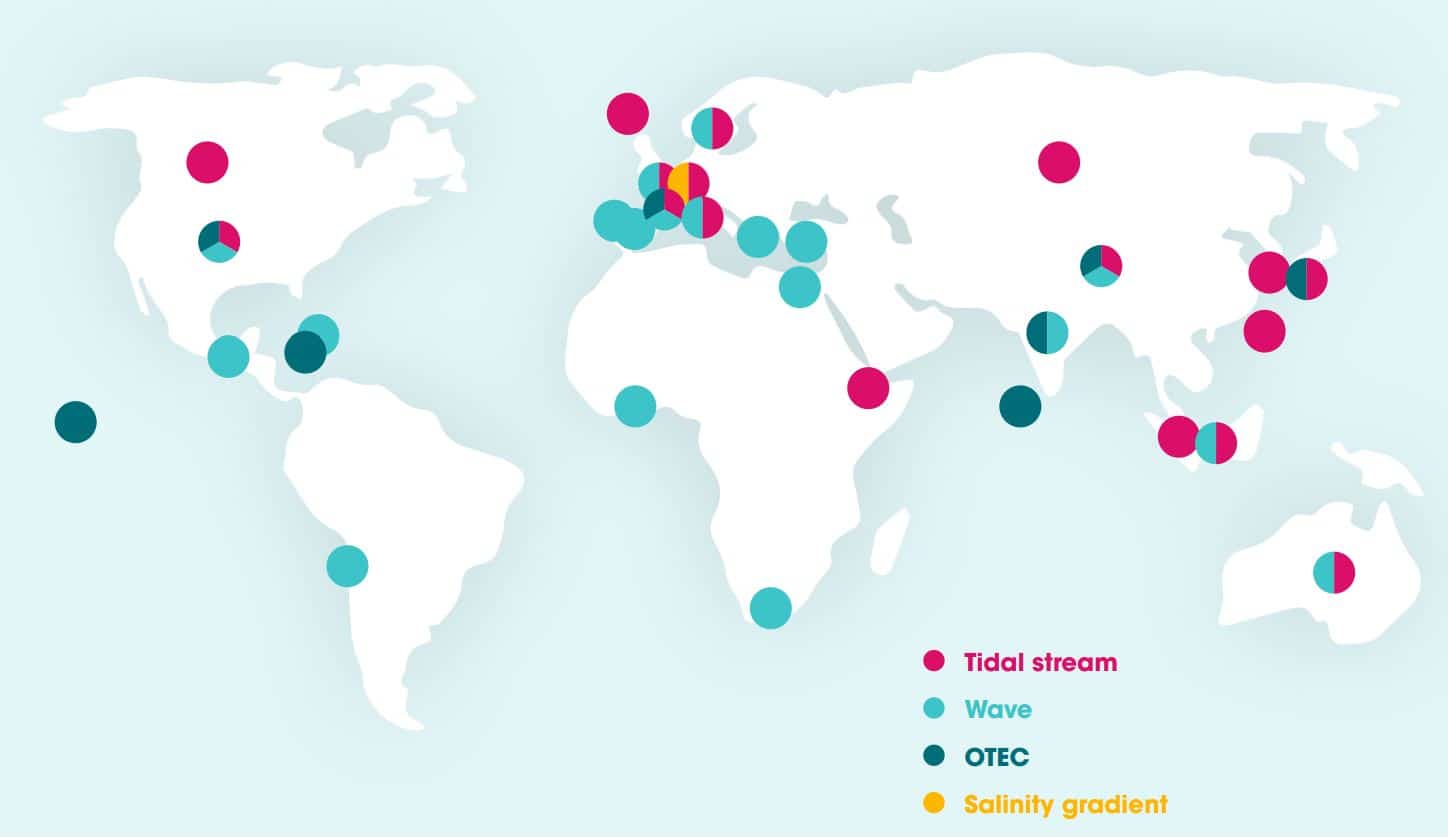

Figure 4: Global distribution of active and projected ocean energy activities

Source: IRENA, 2020c

European countries such as Finland, France, Ireland, Italy, Portugal, Spain, Sweden and the United Kingdom, as well as Australia, Canada and the United States, are today at the forefront of the ocean energy market, with the largest number of projects tested, deployed and planned, as well as most project developers and device manufacturers. While Canada announced in 2020 the support of its first floating tidal energy array of 9 MW in Nova Scotia (Renews, 2020), the European Commission aims at retaining its leadership with the new Strategy on Offshore Renewable Energy of 19 November 2020, a key element of the European Green Deal which lies at the basis of the COVID-19 recovery package (European Commission, 2020) and has ambitious plans for ocean energy:

- 1-3 GW of wave and tidal energy by 2030; and

- 60 GW of wave and tidal energy by 2050.

However, increasing interest is observed in many other locations outside the current markets, predominantly in China, Japan and the Republic of Korea.

The way forward

For ocean energy technologies to materialize, gain visibility, mobilize existent supply chains and create new ones, supportive policy and regulatory frameworks need to be in place which could be facilitated through the following actions (IRENA, 2020c):

- Enhance the business case through innovative models: since most ocean energy technologies are prototypes with just a selection of pilot projects beginning to reach commercialisation, innovative business models – like coupling other offshore markets of the blue economy with ocean energy technologies, or coupling these with variable renewable energy sources – R&D support and increased deployment could help bring costs down, and increase revenues.

- Improve access to finance through ‘blended finance’ principles: adopting blended finance principles. i.e. combining public and private mechanisms while providing both returns on investments and wider social welfare gains, could provide the necessary financial support needed for ocean energy technologies to reach markets faster.

- Strengthen marine spatial planning: unless policymakers are aware of the resource potential of oceans, these technologies will probably remain a niche. Spatial marine planning, in combination with thorough social, economic and environmental impact assessments, accompanied by power grid integration studies could help materialize these technologies.

- Build supply chains thanks to conventional offshore activities: given the current lack of supply chains, synergies among different offshore industries could be leveraged for the deployment of ocean energy technologies, including lessons learned from the conventional oil and gas industry, as well as the offshore wind sector, since all of these had to overcome similar challenges in the past (e.g. supplying sensors, subsea cabling, mooring, etc).

- Include ocean energy technologies into national energy policies: policymakers could improve the policy and regulatory frameworks for ocean energy technologies by acknowledging that these technologies can help achieve national energy targets, including Nationally Determined Contributions (NDCs) under the Paris Agreement (UNFCCC, 2021) and National Renewable Energy Action Plans (NREAPs) within the European Union (European Commission, 2021).

- Improved technological reliability and efficiency to minimize risks: despite recent technological progress, ocean energy technologies need to improve. Tidal energy needs to be scaled up to reduce costs and prove viability, while wave energy would need to converge towards a smaller number of prototypes. International standards and ‘stage-gate’ metrics, i.e. breaking down the innovation process into stages from idea to deployment would bring value.

- Develop capacity through international cooperation: because of the nascent character of the ocean energy industry, capacity building through international cooperation among policymakers, industry, academia and end-users is key. Knowledge exchange among offshore renewables, reskilling the fossil fuel workforce into renewables, and collaborating with academia to prepare the youth for the future needs of the job market are ingredients that can lead to the successful deployment of these technologies.

In this context, following its 10th Assembly in 2020, IRENA created at the requests of its members a Collaborative Framework on Ocean Energy/Offshore Renewables, which met twice in 2020. In addition to the 40 delegations from IRENA’s membership, private sector representatives like the Global Wind Energy Council (GWEC) and Ocean Energy Europe (OEE) have participated actively in the discussions. To bring ocean energy technologies closer to commercialisation, further engagement is planned in 2021 with the G20 and thorough preparation of the agenda for the next major global climate conference, the 26th Conference of Parties to the United Nations Framework Convention on Climate Change (COP26).

About the Author

Elena Ocenic has hands-on experience in solar photovoltaic project development and expertise in European electricity market regulation. Since 2019 she is exploring how innovations in enabling technologies, business models, market design and system operation can help IRENA members achieve their ambitious renewable power policy goals by mid-century. Her analytical work includes tailor-made innovative solutions to achieve up to 100% renewable power by 2050, smart strategies for the electrification of end-use sectors via renewable power-to-X, pathways to decarbonize the industry, as well as the status and outlook of ocean energy technologies.

Elena Ocenic has hands-on experience in solar photovoltaic project development and expertise in European electricity market regulation. Since 2019 she is exploring how innovations in enabling technologies, business models, market design and system operation can help IRENA members achieve their ambitious renewable power policy goals by mid-century. Her analytical work includes tailor-made innovative solutions to achieve up to 100% renewable power by 2050, smart strategies for the electrification of end-use sectors via renewable power-to-X, pathways to decarbonize the industry, as well as the status and outlook of ocean energy technologies.

She has gathered over 10 years of professional experience in international organisations (IRENA, IAEA), European institutions (ACER, European Parliament), the private sector (renewable energy), academia (Sciences Po Paris, Heidelberg University) and NGOs, including French, German and Romanian associations. She graduated with a Master degree in International Economic Policy focusing on Energy from Sciences Po Paris (France) and a Bachelor degree in Political Science and Economics from the University of Heidelberg (Germany). She speaks fluently Romanian, German, English and French.

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights

More on the topic