Negative prices for electricity

Written by S. Ambec and C. Crampes (Toulouse School of Economics)

When we witness producers paying consumers to offload their power, we can but wonder if the relationship between the electricity industry and the market economy is like mixing oil and water. Indeed, the negative prices occasionally seen in electricity exchanges in Europe and the USA are a clear sign to industry players that there is a significant production surplus. However repeated negative prices are mostly attributable to the priority treatment afforded to intermittent renewable energies.

Supply, demand and market equilibrium

Micro-economics teaches us that equilibrium is achieved on a competitive market when supply (increasing relationship between price and quantities) is equal to demand (decreasing relationship between price and quantities). At the equilibrium price paid by buyers, sellers cover production costs as a minimum, and even earn a profit. As supply more or less reflects the cost of production, and as this cost is positive (nothing is free on earth), the meeting point between supply and demand should be a positive price.

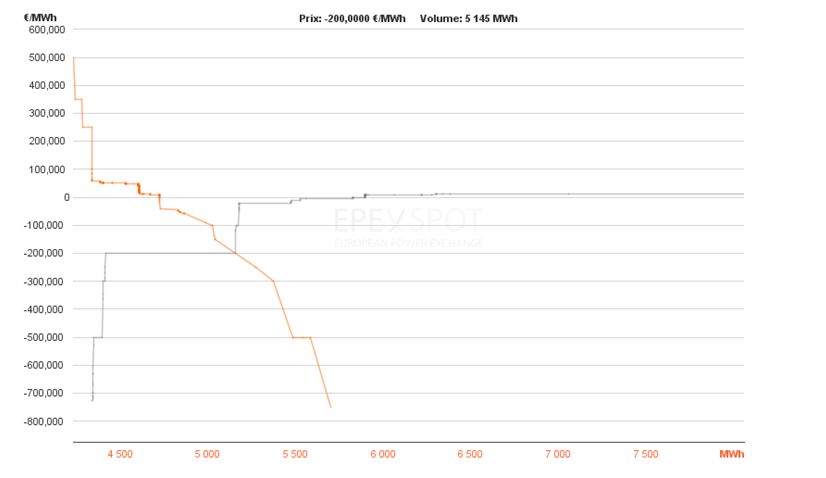

However, on the electricity markets, day-ahead markets (8760 markets per year) and intra-day markets, we can occasionally see that supply and demand intersect at a negative price, like in the attached graph where we can see the French market balancing at a price equal to -€200/MWh on 16 June 2013.[1] To get to this point, certain producers and consumers had to announce their intent to arrange transactions at negative prices.

There is no shortage of willing consumers. If the mayor of a city can light the streets and public spaces whilst boosting the local coffers, if the operator of a pumped storage power station can earn money whilst filling their reservoirs, if a high-cost electricity producer can meet its commitments by charging to use energy produced by others, if we can earn a little extra by cranking the heating up to max (nobody will come and check that we’ve left the windows open) – why not do it?

With regards to electricity sellers, the explanation is less simple: it is mainly due to the inability to store electricity, the lack of flexibility of thermal power plants and payment methods for intermittent renewable energies.

What should we do with production surpluses?

In any industry, when the price goes below the production costs, the producers halt operations. If this interruption does not stop the product flow – which, for example, is the case for crops which are linked to natural cycles – it is stored to wait for better days, or the production surplus is simply destroyed. But storage and destruction have a cost. If we can find consumers willing to increase their consumption for payment lower than the cost of destruction (or the cost of storage, net of future expected sales), it is in the interest of the producers to pay these consumers.

When it comes to get rid of surpluses, the electricity industry experiences combined difficulties: large-scale storage is still impossible (except for pumping stations, but their reservoirs have a limited capacity), and surpluses can only be exported up to interconnection capacities and provided that the interconnected countries do not have a production surplus themselves. A willingness to pay consumers to absorb energy surpluses fed into the network could therefore be the logical conclusion of an economic calculation. But where do these surpluses come from?

Why are there production surpluses?

Electricity production must adapt to ongoing demand which varies day-by-day, hour-by-hour and based on weather conditions. Production must therefore be flexible, both upwards and downwards. Intermittent energies (solar, wind, run-of-river) depend fully on immediate natural supplies. They are therefore only flexible downwards by disconnecting production units. On the contrary, hydroelectric power from dams & reservoirs is completely flexible. Between these extremes, thermal power plants have a flexibility which varies based on prescribed timeframes.[2] As car drivers are well aware, you can’t switch instantly between a stop and 50 mph, nor between 50 mph and a stop, nor between 50 and 60 mph, etc. There is ongoing acceleration and deceleration, i.e. dynamic management of car combustion engines, like electricity plants using fossil fuels.

Therefore, in thermal power plants, the chosen production for one given hour does not solely depend on the market conditions during that hour. The production status during the previous hours and the forecasts for the following hours also play an essential role. If, for example, the operator of a thermal power plant thinks it will have to produce a lot of energy between 7am and 8am and if, to meet this demand, they must start to increase production as of 4am, they need to be sure that their power plant will be called by the market operator at each hour between 4am and 7am. The economic cost of MWh produced during the night is therefore lower than the immediate marginal cost, as we need to deduct the expected gains at peak hours thanks to the ramp-up during the night. This deduction can be so significant that the economic cost of night-time hours becomes negative. It is this value – lower than the immediate marginal cost, and possibly negative – which will be presented as a bid by the operator of the thermal power plant. We can therefore interpret the negative price offered during off-peak night-time hours as an investment intended to increase gains during peak morning hours.

From bids to price

However, negative bids by thermal power plant operators are not sufficient to reach negative equilibrium prices.[3] Offering to sell at a negative price first increases the chances that the offer will be accepted by the market operator, by being the lowest bidder amongst other bidders. The actual price received by all dispatched producers will be the equilibrium price, which has a good chance of being positive… except if i) the demand is very low and ii) the supply is very high. This is what we can see in the example illustrating this post where the decreasing demand curve (in red) is located to the far left and the growing supply curve (in blue) to the far right of the graph.

This is where regulation is involved, which encourages the feeding of renewable energies into electrical networks. For these forms of energy, the ramp-up argument indicated previously does not hold. So why do the producers who use these primary energies present negative bids on the markets, at the risk of the equilibrium price being negative, and therefore below their variable production cost which is close to zero? Because they are rewarded with positive regulated purchase prices (the so-called feed-in tariffs) or premiums, and they have priority dispatching as ruled by the system operator (in France, RTE)… if they produce. As a result, their economic cost, calculated by subtracting the premium support tariff from the immediate zero cost, is negative. Let’s look at it differently: i) if my output is not accepted by the market operator, I earn 0; ii) if it is, I earn the regulated purchase price;[4] iii) I therefore want my output to be called by the dispatcher if the negative bid is lower in absolute value than equal to the absolute value of the price premium. In western Europe, the more wind output at off-peak hours during the night, together with surplus output due to a ramp-up of thermal power plants in preparation for the morning peak hours, the greater the chance of negative prices before dawn’s first light.[5]

Competition and efficiency

Renewable energy subsidies distort competitive mechanisms, but they are state aid exempted from the prohibition regime by the European authorities as they help de-carbonise the electricity industry. An economist cannot just accept that they are part of the energy transition without first asking what they cost and if there are other solutions which are at least as effective and cheaper.

The best solution – a familiar one but one which political leaders do not wish to apply due to its “punitive” nature – is a CO2 price acting as a marker for investment, production and consumption decisions, and reflecting the marginal damage of greenhouse gas emissions. The specific promotion of renewable energies of any kind increases the cost of attempts to reduce greenhouse gases by making the development of renewable energies an objective instead of one resource amongst many.

As part of the problem which we are looking at here, and by limiting ourselves to the European Union, renewable subsidies have a drawback in that they place wind output before thermal power plants in the merit order for certain off-peak hours, regardless of the requirements in the following peak hours.

What should be the merit order? If there is a lot of wind at night, and there is also strong wind predicted during morning peak hours, enough to satisfy most demand, it is efficient to feed the original wind power electricity into the network at night and in the morning. By contrast, if there is a lot of wind at night but low winds predicted in the morning, we must prioritise energy produced by thermal power units at night, so that they ramp up and are operational in effective conditions in the early hours of the morning.

It is not difficult to obtain this result. We just need to ensure that bids presented on electricity exchanges reflect the economic operating cost, excluding subsidies. The bids submitted to the auction would therefore be: i) for wind farms, always €0; ii) for thermal power plants, a value lower than the immediate cost (and possibly negative) when they are in a ramp-up or ramp-down phase, and a bid equal to their immediate marginal cost when producing in stationary conditions.

The priority places would therefore be given either to zero-price bids (presented by wind farms) followed by positive prices at times when thermal power plants are not dealing with excessive dynamic constraints, or negative price bids (presented by thermal power plants) followed by zero prices from wind farm operators when thermal power plant operators need to feed more into the network than immediate requirements. If demand is very low, dispatching may require that some wind output is not fed into the network. The merit order would therefore reflect the efficient ranking of technologies in a dynamic context, rather than a static one.

* * *

If the current system is maintained, there will be even more negative prices for electricity as more wind farms are developed.[6] The reform suggested above should reduce the number of negative prices without getting rid of them entirely, which is good for economic efficiency as they indicate that there is excess supply, encouraging output reduction. Nevertheless renewable energies drag prices down, which endangers the financial balance of traditional technologies and reinforces demand by operators of these technologies for means to finance their capacity in addition to the energy produced. In fact, due to their intermittent nature, renewable energies cannot totally replace traditional energies. It is therefore up to us, the consumers/taxpayers, to pay for the installation and maintenance of both types of technologies. And whilst the occasional negative prices drag electricity wholesale prices down, the consumer electricity bill continues to rise to cover the “contributions” required to recoup the cost of each type of producer.

[1] On 16 June 2013, the price started to be negative at 3am, fell to reach -€200/MWh between 5am and 8am, then rose to fluctuate around 0 before falling again in the afternoon. (https://www.epexspot.com/fr/donnees_de_marche/dayaheadfixing/courbes-agregees/auction-aggregated-curve/2013-06-16/FR/05/3).

[2] There are two types of thermal power plant: those which use a steam cycle (coal, natural gas, nuclear fuel) and combustion turbine plants (simple or combined cycle). The second is more flexible than the first.

[3] A glance at www.epexspot.com/fr/donnees_de_marche/dayaheadfixing/courbes-agregees/auction-aggregated-curve/ shows that negative bids are recorded on nearly all hourly markets.

[4] Or the market price plus the green energy premium depending on the regulatory regime.

[5] In California, solar energy peaks during the middle of the day cause negative prices. See http://www.caiso.com/Documents/2016FourthQuarterReport-MarketIssuesandPerformanceMarch2017.pdf, pages 17-18.

[6] In Germany, there were 126 negative price hours in 2015, and 97 in 2016. In France, they can still be counted on one hand.

Don’t miss any update on this topic

Sign up for free and access the latest publications and insights